2023-11-1 04:30:38 Author: blogs.sap.com(查看原文) 阅读量:9 收藏

Citizens concerned about climate change have put governments under pressure in the last few years. Expectations have only grown over time since Nationally Determined Contributions like the Paris Agreement or the creation and monitoring of Sustainable Development Goals, expectations in governments to provide a sustainable environment grew.

Therefore, the International Monetary Fund together with different organizations such as the United Nations Development Program have introduced Green Public Finance Management which should support governments in implementing sustainable development goals into their Public Finance Management Framework

This blog is a summary on the papers:

1: IMF: STAFF Climate NOTES. Climate-Sensitive Management of Public Finances” Green PFM”

2: IPSASB. Advancing Public Sector Sustainability Reporting.

and should show you the applicability of SAP solutions to these concepts.

By integrating climate-related objectives into public financial management and its related framework, Green PFM can be developed, which is a more accurate and efficient approach than green budgeting itself.

A Holistic Approach To Green PFM:

Green Public Finance Management (GPFM) is an innovative approach to fiscal policy and public resource allocation that supports sustainable development objectives. It integrates environmental and climate considerations into all aspects of public finance, from budgeting and procurement to tax policy and debt management. GPFM recognizes that public finance is a key tool for policy implementation, and that the public sector has a crucial role to play in steering economies towards greener and more sustainable trajectories.

Fig. 1: Adapted from source 1: A Holistic Approach to Green Financial Management

As visible in Figure 1, the budget cycle was built along four steps:

1 Strategic planning and fiscal framework

2 Budget and preparation.

3 Budget execution and accounting

4 Control and audit.

All these steps need to be part of a strong and functional PFM framework and only if such a PFM framework already exists will implementation of climate commitment work towards a Green PFM be possible. The starting point of green transformation is therefore an existing strong financial budget along the budget cycle. So that their financial resources are planned, directed, and controlled to enable their intended outcomes (Source 3).

From there green funds can be added, prioritized to add allocated to green initiatives, such as renewable energy, sustainable transport, and nature-based solutions successfully. This could include creating subsidies for clean energy, imposing taxes on carbon emissions, or investing in green infrastructure. It also involves integrating environmental risk assessments into financial decisions and ensuring that public funds do not support environmentally harmful activities. For instance, public pensions or sovereign wealth funds could divest from fossil fuels, or public procurement could favor goods and services with lower environmental footprints.

However, GPFM is not just about the allocation of resources, it is also about promoting transparency and accountability in how public funds are used for environmental purposes. This could involve tracking and reporting on green expenditures or setting up mechanisms to ensure that funds earmarked for green initiatives are used for their intended purpose.

Case – Study: Vienna Climate Budget

Vienna’s commitment to green budgeting for example is evident through its climate budget strategy, which is a proactive approach to address climate-related issues. Annually, decisions are made to select and implement climate-related measures and tools for the upcoming budget year. If necessary, the budget allocation for these measures is also determined. The climate budget process emphasizes a thorough evaluation of proposed measures based on multiple criteria to facilitate informed political decision-making. The goal of this process is to identify a robust set of effective measures and tools for climate protection and adaptation, thereby enabling Vienna to meet its climate objectives within its annual budget (See:Steuerungsstrukturen und -regelungen – Steuerungsstrukturen und -regelungen – Wiener Klimafahrplan).

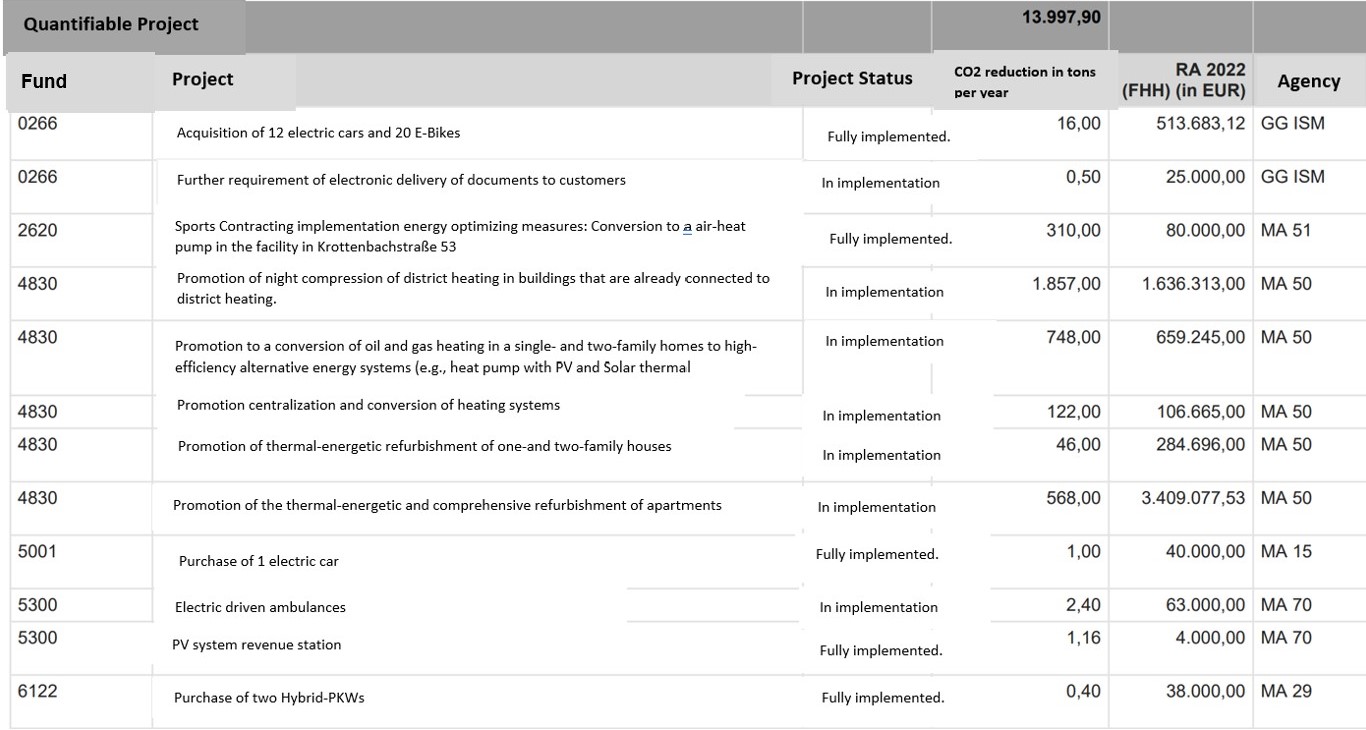

Thus, the annual financial statements indicate the number of tons of emissions reduced in relation to the various projects. This facilitates the evaluation of the budget and its use to get closer to the climate targets. Here is an excerpt from the annual report of 2022 (Figure 2).

Fig. 2: Adapted from Source 3: Rechnungsabschluss der Bundeshauptstadt Wien für das Jahr 2022

This supports Finance Officers conducting cost-benefit analysis more efficiently, which involves an analysis to evaluate the economic and environmental impacts of proposed measures, ensuring that budget allocations are cost-effective and yield positive environmental outcomes.

Vienna’s climate budget aligns with Green Public Finance Management by integrating climate considerations into budget planning, prioritizing climate spending. This includes the conduction of cost-benefit analyses. The climate budget process is transparent, with clear reporting mechanisms in place. This transparency allows citizens and stakeholders to track how public funds are being allocated and spent on climate-related initiatives, promoting transparency and accountability. This alignment helps Vienna effectively manage its finances while advancing its climate and environmental goals (Source 3).

Following the holistic framework, a Green PFM strategy can be used as a powerful tool to successfully pursue sustainability goals. By integrating sustainability into public finance, we can make our economies more resilient, create new jobs and opportunities, and help secure a safe and prosperous future for all.

Learn about Public Sector and IPSASB and how to include the concept of GPFM in SAP solutions in my next blogs, which will be released soon.

Sources:

1: Aydin, Ozlem; Battersby, Brain; Gonguet, Fabien; Wendling, Claude. 2021. IMF: STAFF Climate NOTES. Climate-Sensitive Management of Public Finances-” Green PFM.” Found in: CLNEA2021002.pdf

2: IPSASB. 2022. Advancing Public Sector Sustainability Reporting. Found in: IPSASB-Staff-QA-Climate-Change-Relevant-Guidance.pdf

3: Hanke, Peter. 2023. Rechnungsabschluss der Bundeshauptstadt Wien für das Jahr 2022. Found in: https://www.digital.wienbibliothek.at/wbrup/download/pdf/4615074?originalFilename=true

4: Köppl, Angela; Schleicher, Stefan; Mühlberger, Manfred and Steininger Karl W. 2020. Klimabudget Wien. Klimaindikatoren im Rahmen eines Klimabudget. Found in: https://www.wifo.ac.at/jart/prj3/wifo/resources/person_dokument/person_dokument.jart?publikationsid=66396&mime_type=application/pdf

Additional SAP Links that could also be interesting:

SAP Sustainability Navigator (ondemand.com)

SAP Sustainability Control Tower

Green Ledger: Where Carbon and Financial Accounting Unite (sap.com)

https://roadmaps.sap.com/board?range=CURRENT-LAST&FT=SUSTAINABLE#Q1%202024

如有侵权请联系:admin#unsafe.sh