Dealing with Missing Data in Financial Time Series - Recipes and Pitfalls

2024-4-3 23:3:8 Author: hackernoon.com(查看原文) 阅读量:2 收藏

2024-4-3 23:3:8 Author: hackernoon.com(查看原文) 阅读量:2 收藏

Too Long; Didn't Read

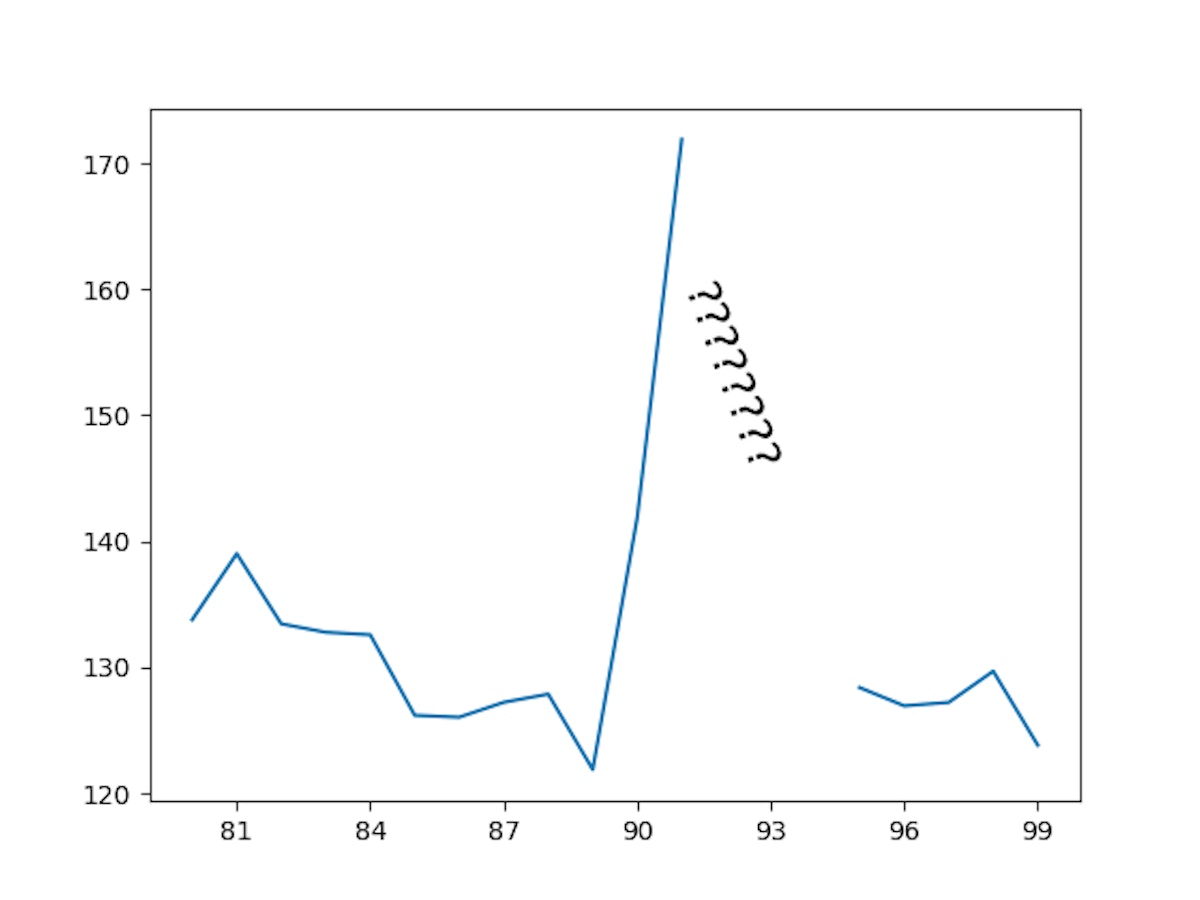

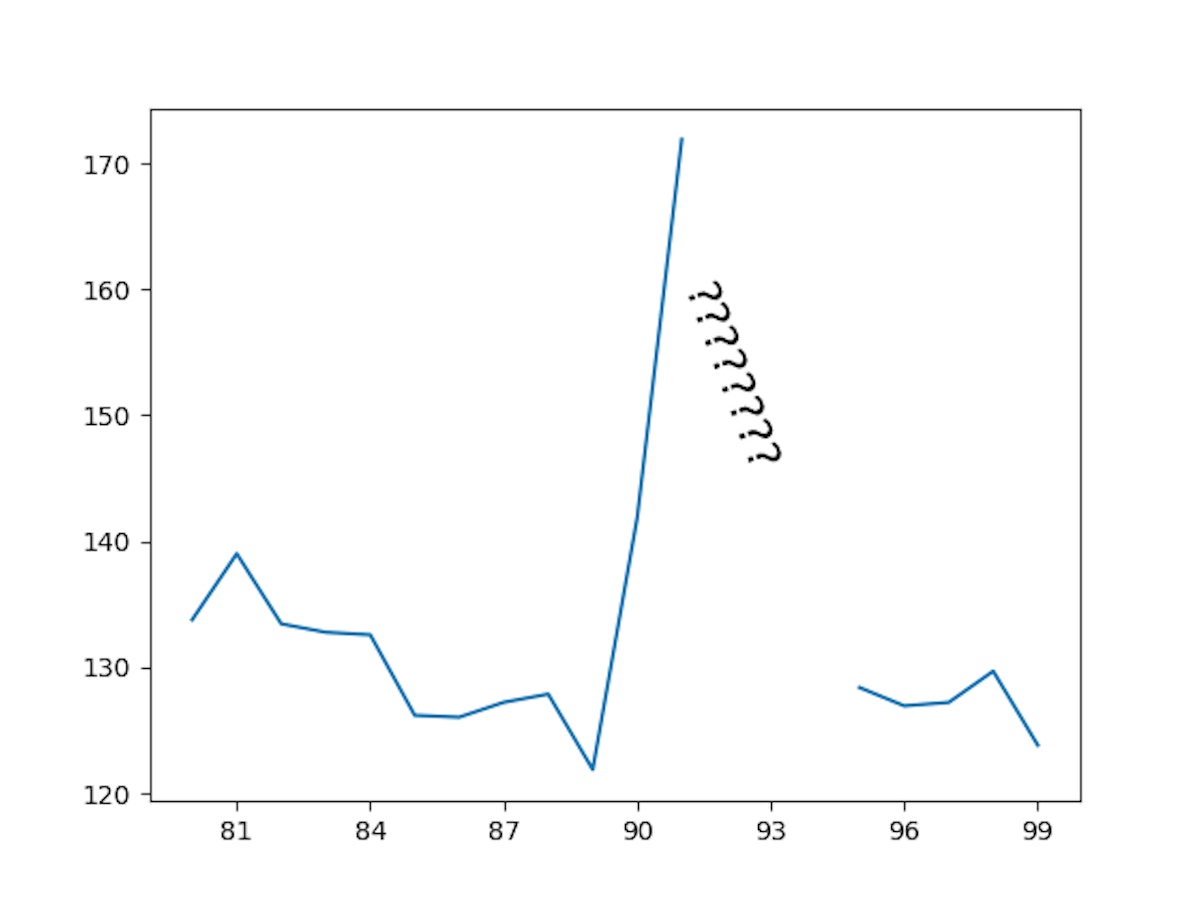

I focus on methods to handle missing data in financial time series. Using some some example data I show that LOCF is usually a decent go-to method compared to dropping and imputation but has its faults - i.e. can create artificial undesirable jumps in data. However, alternatives like interpolation have their own problems especially in context of live prediction/forecasting.

Vladimir Kirilin

@hackerclrk2ky7l00003j6qwtumiz7c

Quant @ Five Rings Capital

STORY’S CREDIBILITY

Opinion piece / Thought Leadership

The is an opinion piece based on the author’s POV and does not necessarily reflect the views of HackerNoon.

About Author

Quant @ Five Rings Capital

L O A D I N G

. . . comments & more!

TOPICS

Languages

THIS ARTICLE WAS FEATURED IN...

RELATED STORIES

文章来源: https://hackernoon.com/dealing-with-missing-data-in-financial-time-series-recipes-and-pitfalls?source=rss

如有侵权请联系:admin#unsafe.sh

如有侵权请联系:admin#unsafe.sh